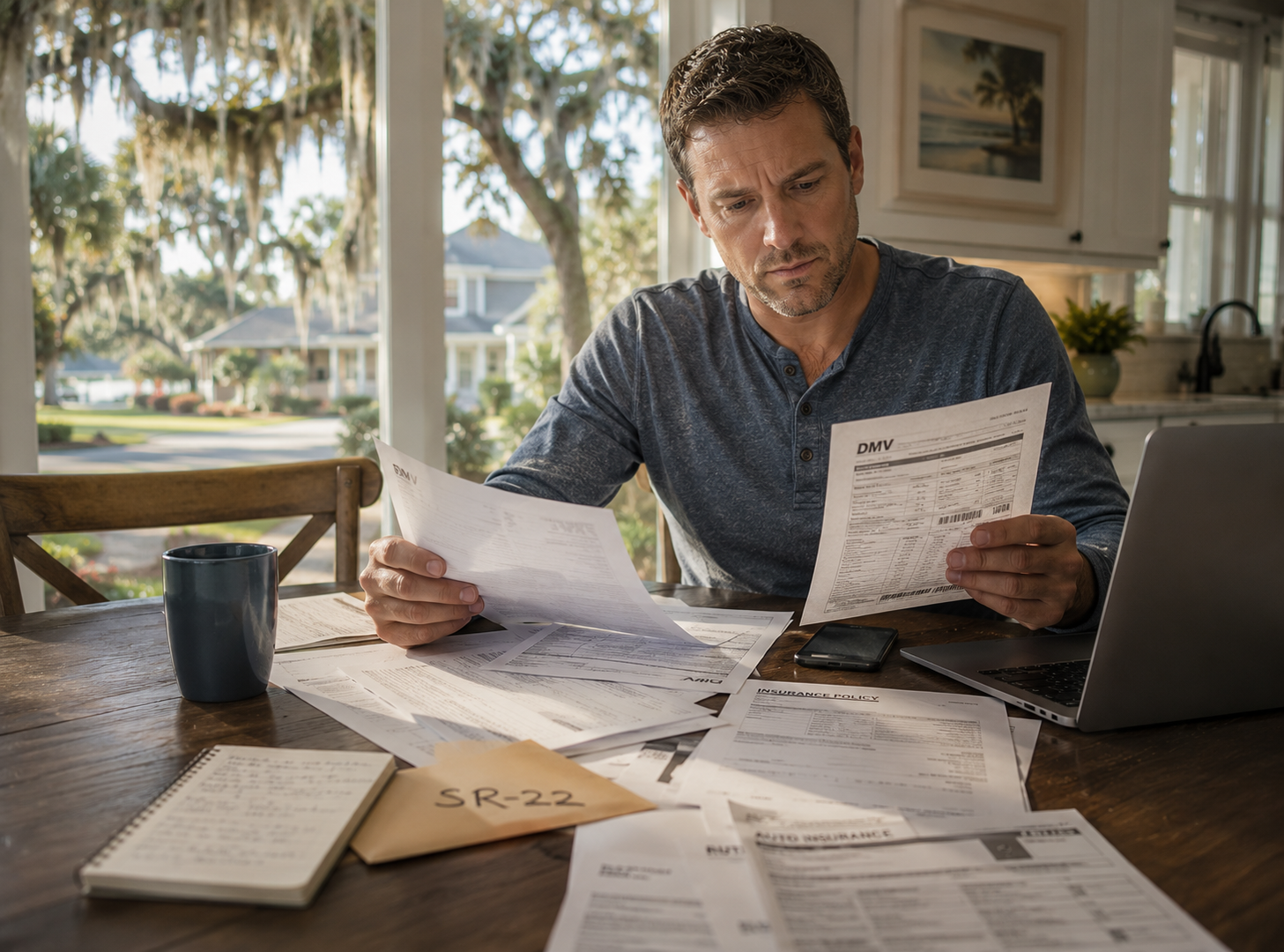

How Do I Get SR-22 Insurance in South Carolina?

Quick Answer:

To get SR-22 insurance in South Carolina, you need to purchase an auto insurance policy from a company that offers SR-22 filings and have that insurer submit the SR-22 certificate directly to the South Carolina DMV. An SR-22 is not a separate type of insurance, it is proof that you carry the required liability coverage after situations such as a license suspension, DUI, uninsured driving violation, or other serious driving-related offense.

Most people searching for SR-22 insurance are not casually shopping for coverage. They are trying to solve a problem that already feels urgent.

A license may be suspended. A court deadline may be approaching. Someone may need to drive legally again to keep a job, take care of family responsibilities, or simply regain some normalcy after a difficult situation. For many South Carolina drivers, the phrase “SR-22” appears during one of the most stressful periods they have ever experienced involving insurance or the DMV.

At Coastal Haven Insurance, we understand that people dealing with SR-22 requirements are usually trying to move forward, not become experts in insurance terminology overnight.

That is why this process needs to be explained clearly and honestly.

An SR-22 is not a special insurance policy by itself, and it is not a driver’s license. It is a filing submitted by your insurance company to the South Carolina DMV showing that you carry the state-required liability insurance coverage. The filing exists so the state can monitor whether your policy remains active during the required compliance period.

And for many drivers, the hardest part is not getting the SR-22 filed. The hardest part is maintaining stable coverage long enough to avoid another suspension or compliance problem later.

What Is an SR-22 in South Carolina?

An SR-22 is a certificate of financial responsibility filed by an insurance company with the South Carolina DMV. It proves that a driver has active liability insurance meeting South Carolina’s minimum insurance requirements.

One of the biggest misunderstandings surrounding SR-22 insurance is believing the SR-22 itself is an insurance policy. It is not. You still need an actual auto insurance policy first. The SR-22 filing is then attached to that policy so the DMV can verify that coverage stays active.

Drivers are commonly required to carry an SR-22 after situations involving DUI-related offenses, uninsured driving, license suspension, reckless driving incidents, repeat traffic violations, or other serious driving-related problems that trigger financial responsibility requirements with the state.

This is also where confusion often begins.

The court, the DMV, and the insurance company may all be involved in the process, but they are not handling the same responsibility. The court may establish legal requirements connected to the violation. The DMV controls license reinstatement and compliance. The insurance company provides the policy and files the SR-22 certificate with the state.

When drivers misunderstand which step comes next or assume one agency handles everything automatically, delays and compliance issues happen quickly.

Why the SR-22 Process Feels So Confusing

Most drivers dealing with an SR-22 situation are already overwhelmed before they even begin shopping for insurance.

They may be juggling DMV notices, court paperwork, suspended-license concerns, rising insurance costs, reinstatement fees, and pressure from work or family obligations all at the same time. Many people are hearing unfamiliar terminology for the first time while trying to solve the problem as quickly as possible.

That is why the process feels so frustrating.

One person says the DMV needs proof of insurance. Another says the court requirement is separate. Online quote systems may not clearly explain whether the SR-22 filing is actually included. Some drivers purchase a policy believing everything is complete, only to later discover the DMV never received the filing correctly.

Others assume that once the license becomes active again, the SR-22 requirement automatically disappears.

Unfortunately, that misunderstanding often creates a second wave of problems months later.

Most drivers assume the hardest part is getting the SR-22 filed. In reality, the bigger challenge is maintaining continuous coverage long enough to satisfy the state requirement without another lapse or suspension issue interrupting the process.

How Do You Get SR-22 Insurance in South Carolina?

The process usually begins by confirming exactly what the South Carolina DMV or court requires for your situation.

Before purchasing coverage, drivers need to understand whether they need an owner policy, a non-owner policy, a reinstatement filing, or another specific form of compliance tied to their record.

After that, the next step is finding an insurance company willing to provide SR-22 filing. Not every carrier offers SR-22 filings, and many preferred insurance companies may decline drivers with recent serious violations or suspension-related histories.

This is one reason many drivers become frustrated with online quote systems. Some websites advertise low pricing quickly but fail to explain whether the SR-22 filing is actually included or whether the driver fully qualifies after underwriting review.

Once the policy is issued, the insurance company files the SR-22 certificate with the South Carolina DMV. Drivers should then verify that the DMV processed the filing correctly and that any remaining reinstatement fees or compliance requirements have been completed before driving again.

That final verification matters tremendously.

A driver can purchase insurance and still not be legally reinstated yet. Driving before the reinstatement process is fully completed can create another violation very quickly.

How Long Does the SR-22 Process Usually Take?

Many South Carolina SR-22 filings can be submitted electronically the same day the policy becomes active, although DMV processing and reinstatement timing can still vary depending on the situation.

That timing difference creates a great deal of confusion for drivers trying to get back on the road quickly.

Some people assume that once they buy the policy, they are immediately legal to drive again. Others expect the DMV update to happen instantly. In reality, there can still be processing delays tied to reinstatement requirements, outstanding fees, or compliance verification.

This is why confirmation matters.

Drivers should verify that the SR-22 filing was submitted correctly, processed by the DMV, and fully connected to an officially reinstated license status before driving again.

Many costly mistakes happen during the small gap between purchasing the policy and fully restoring legal driving privileges.

What Happens After a DUI Insurance Requirement in South Carolina?

DUI-related SR-22 situations are often where drivers experience the most dramatic insurance changes.

A DUI conviction can move someone into a much higher-risk underwriting category almost immediately. Preferred carriers may refuse renewal, premiums often increase substantially, and available insurance options can narrow very quickly.

For many South Carolina drivers, this creates financial pressure on top of an already stressful legal situation.

A driver commuting daily through Bluffton on Highway 278, a hospitality employee traveling to Hilton Head resorts, or a construction worker driving across Beaufort or Jasper County may suddenly realize that losing driving privileges threatens employment directly.

That urgency is real.

In many parts of South Carolina, especially Bluffton, Beaufort, rural Lowcountry communities, and long commuter corridors across the state, driving is not optional. Public transportation options are limited, and many households depend heavily on personal vehicles for work, childcare, school transportation, and daily responsibilities.

That reality is one reason SR-22 situations feel emotionally overwhelming for many people. They are often trying to solve transportation, legal, financial, and employment problems simultaneously.

Can You Get SR-22 Insurance Without a Car?

Yes, some South Carolina drivers may qualify for a non-owner SR-22 policy if they do not own a vehicle but still need to satisfy a state filing requirement.

A non-owner policy generally provides liability coverage for someone who does not own a vehicle but occasionally drives vehicles they do not own.

This can help drivers reinstate a license even if they currently do not have a personal car.

However, non-owner coverage is frequently misunderstood.

If someone owns a vehicle, regularly drives a household vehicle, or consistently has access to a car they use frequently, a non-owner policy may not properly fit the situation. Buying the wrong policy type simply because it appears cheaper can create serious coverage issues later if an accident occurs.

We regularly see drivers searching for “cheap non-owner SR-22 insurance” without fully understanding whether the policy actually matches how they drive in real life.

The goal should not simply be finding the lowest payment possible. The goal should be finding coverage that legally and realistically matches the driver’s actual exposure.

Why SR-22 Insurance Costs More

The SR-22 filing itself is usually not the expensive part.

The larger cost typically comes from the driving history or violation connected to the filing requirement. DUI convictions, uninsured driving citations, suspended licenses, repeat traffic violations, prior accidents, and insurance lapses all increase underwriting risk from the insurer’s perspective.

That higher-risk classification often leads to fewer carrier options, larger down payments, higher monthly premiums, and more restrictive underwriting conditions overall.

Pricing can also vary significantly depending on age, location, vehicle type, prior insurance continuity, driving history, and credit-related underwriting factors.

A young driver in Columbia, a commuter in Charleston, a service worker in Bluffton, and a driver living in a rural South Carolina community may all receive dramatically different SR-22 pricing even if each requires the same filing.

This is another reason online quote systems can become misleading. The initial number shown online is not always the final underwriting result.

Why the Cheapest SR-22 Policy Is Not Always the Safest Option

This is one of the most important parts of the entire process.

Many drivers understandably search for the absolute cheapest SR-22 insurance possible because the situation already feels financially overwhelming. But some low-cost policies create additional risk if the billing structure is unstable, the down payment is unrealistic, or the carrier cancels aggressively after missed payments.

An SR-22 lapse is not simply an insurance problem.

It can quickly become another DMV problem.

We regularly see drivers focus entirely on lowering the monthly payment while underestimating the importance of stability, communication, billing reliability, and continuous compliance.

A policy that barely stays active for one or two months can become far more expensive if it triggers another suspension cycle afterward.

The better question is often not, “What is the cheapest SR-22 policy?”

The better question is, “What policy can realistically stay active long enough to complete the requirement successfully?”

The Biggest SR-22 Problem Usually Happens Months Later

Most SR-22 problems do not happen on the day the filing is submitted.

They happen later.

A payment gets missed during financial hardship. A cancellation notice gets overlooked. A driver switches insurance companies without proper overlap. Someone assumes the requirement ended automatically after reinstatement.

Then the policy lapses.

Because SR-22 compliance depends on continuous insurance coverage, the insurance company may notify the South Carolina DMV about the cancellation. That can trigger another suspension, additional reinstatement fees, longer compliance periods, and even higher future insurance costs.

We have seen situations where the original violation created the SR-22 requirement, but the later policy lapse created the far more damaging long-term problem.

That is why rebuilding stability matters so much.

Setting up automatic payments, maintaining updated contact information, reviewing billing schedules carefully, and avoiding unnecessary coverage gaps are often more important than drivers initially realize.

The Goal Is Not Just Filing Paperwork — It’s Rebuilding Stability

SR-22 insurance is not simply about satisfying a state form requirement.

For many drivers, it is part of rebuilding stability after a difficult period involving financial pressure, driving violations, insurance lapses, or legal problems.

Most people searching for SR-22 insurance are simply trying to get legal, get back to work, take care of their families, and move forward.

That is why the process should be approached strategically rather than reactively.

Continuous coverage matters. Avoiding another lapse matters. Choosing the correct policy structure matters. Understanding the timeline matters. Rebuilding a stronger insurance position over time matters.

At Coastal Haven Insurance, we approach SR-22 situations with clarity and respect because most people already feel enough pressure before they ever make the call.

As an independent agency, we are not tied to a single carrier’s underwriting rules. That matters because some insurance companies will not handle SR-22 filings at all, while others may offer more stable options for drivers rebuilding after a suspension or serious violation.

The right guidance can help drivers avoid compliance mistakes, maintain legal driving privileges, and create a more stable path forward instead of repeating the same cycle again later.

The Real Risk Is Thinking the Filing Is the Finish Line

Getting an SR-22 filed is important, but it is not the end of the process.

The real challenge is maintaining continuous coverage, avoiding additional violations, satisfying the state requirement completely, and rebuilding a healthier insurance profile over time.

Drivers who treat the SR-22 as a one-time form often end up facing the same problems again months later.

A better approach is viewing the SR-22 period as a rebuilding phase. Maintain stable coverage. Avoid missed payments. Confirm DMV compliance carefully. Review policy changes before switching carriers. Make sure the insurance structure actually matches how you drive.

If you need SR-22 insurance in South Carolina, Coastal Haven Insurance can help you understand your options, find a carrier capable of handling the required filing, and structure coverage with the goal of helping you get legal and stay legal.